In a previous article we touched on the 4% rule. The 4% rule takes the idea of multiplying your annual expenses by 25 to deteremine how much money you will need to sustain your retirement. If you currently need $32,000 to cover all of your bills and expenses you will multiply that by 25 giving you your financial independence number of $800,000. If you reach $800,000 and only withdraw 4% each year you should theoretically never run out of money. As with everything in life there are exceptions, but this is a well researched rule that has become somewhat of the standard among those looking to become financially independent.

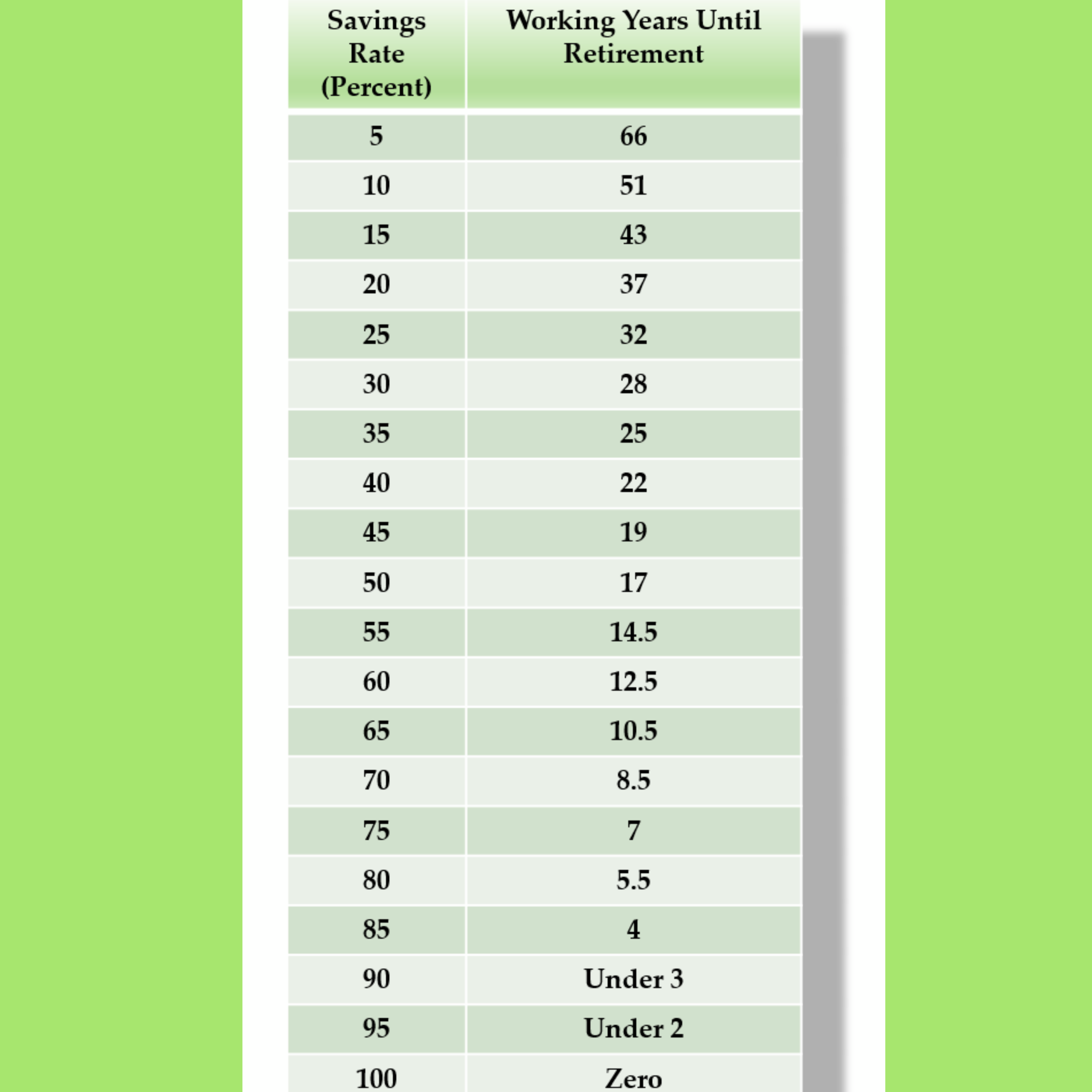

You might be thinking- Wow, $800,000 seems like a lot of money. How long will it take me before I hit that goal? Luckily many charts have been created and the one I have used to determine my FI number was created by Mr. Money Mustache in one of his most famous articles “The shockingly simple math behind early retirement.”

Here’s a link to that article: www.mrmoneymustache.com/2012/01/13/the-shockingly-simple-math-behind-early-retirement/.

The above chart illustrates how many years it will take before you are able to reach financial freedom. The amount i like to reach for is the 65-70% number. This means if I save 65% of my income I will be self sufficient and not depend on work any longer after 10.5 years. If I bump that up to 70% it will only take 8.5 years. This is why it is a great practice to put your savings on auto pilot. If I automatically budget to save 70% of my income and spend the left over 30% on my needed expenses, I know in my head that I will be able to reach financial independence in 8.5 years.

The great thing about this chart is that it works with percentages, meaning your income really doesn’t matter. Whether you make $500,000 per year or $50,000 per year the time it will take you to reach your financial independence number soley depends on how much you save, not how much you make per year.

A couple things to consider:

1. Should I count my home equity towards my financial independence number?

My opinion is that you should not. A lot of people like to include home equity when they are crunching the numbers to determine when they are financially independent. The only problem with a home is that it is no where near as liquid as cash or investments and unless you plan on selling your home and doing something with the equity you have put into it, it becomes a stagnant part of your portfolio that generally isnt earning you money. A quick example of this may be a young couple who is looking to become financially independent. They live in a high cost of living area but have paid off their 400k home and have no debt. The couple determines that they can live off of $24,000 per year as they don’t spend much and no longer have a mortgage. This couple has $200,000 in investments and cash leaving them with a net worth of $600,000. Now here is where the problem comes in. In order to withdraw this $24,000 per year, this couple needs $600,000 of cashflow that they can withdraw from. But they have only $200,000 in investments and cash meaning that by withdrawing $24,000 per year they will run out of money in approx. 10 years. By not including their home equity the couple will now realize that they need to save $600,000 that does not include their home in order to sustain a $24,000 withdrawal every year for the rest of their life.

So to make things simple, do not include your home equity in your early retirement number unless you have plans to sell that home and invest the cash you receive from the sale in some shape or form.

2. Do 401k contributions count since they are pre tax?

Yes, they do. When determining your savings rate you should include all money that your are setting aside for retirement whether it be in a 401k, pension fund, 457b, Roth IRA, etc. All of these accounts contain money you are saving and should be included when determining your savings rate.

So my advice to you is to review the chart above often. Take a picture of it and put it in your phone and constantly remind yourself that the more you increase your savings rate the sooner you will be able to reach financial independence or early retirement. Realize that every extra dollar you save will reduce the time you have to continue working. And lastly enjoy the journey. Enjoy challenging yourself to save money and enjoy watching those investment accounts grow.

-Matt-

Great read as always!

LikeLike